2026 State of the Workplace report reveals true market conditions

Job insecurity and polarised demand amount to a disorienting, sluggish job market. That’s what this year’s research found, published in the 2025/2026 annual Keegan Adams Financial Services Talent and Employment Report. Fear is driving an asymmetric job market, but forces are reshaping historic candidate movements, precipitating migration to smaller firms. Meanwhile, demand for very specific…

Published on June 3, 2026

Job insecurity and polarised demand amount to a disorienting, sluggish job market. That’s what this year’s research found, published in the 2025/2026 annual Keegan Adams Financial Services Talent and Employment Report.

Fear is driving an asymmetric job market, but forces are reshaping historic candidate movements, precipitating migration to smaller firms. Meanwhile, demand for very specific skills is high.

- Tenures have lengthened driven by job security fears: Job security is now workers number one concern. Reversing the trend of previous years, workers expect to stay an average 42% longer in their current role than in 2023. More than double those of 2024 expect to stay 5yrs or longer

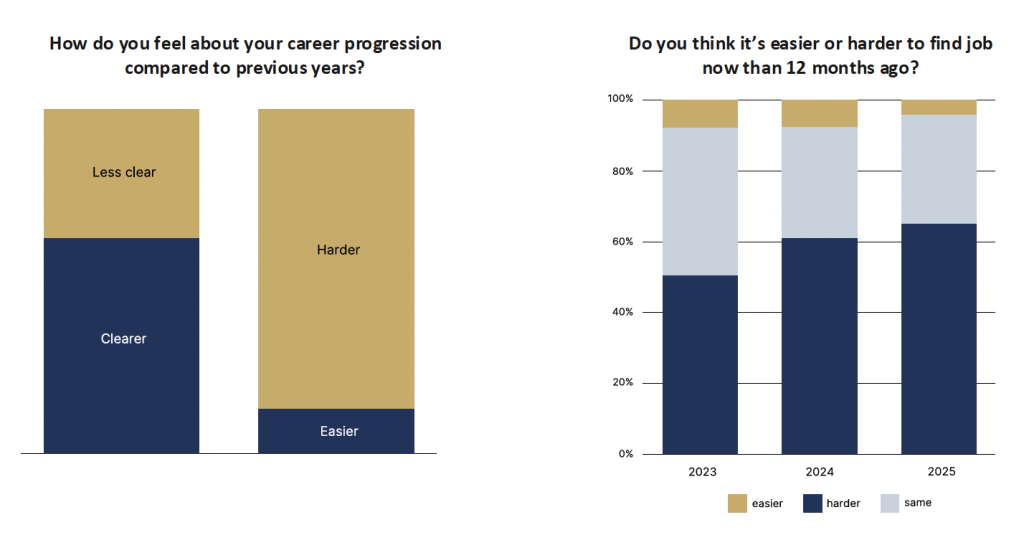

- Finding a job is tough: over two thirds say it’s harder than a year ago

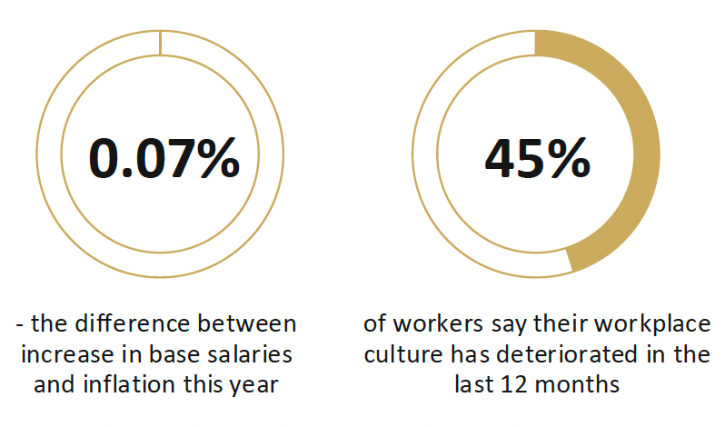

- Salaries remain in total stagnation: the average increase is just 0.07% above inflation

- But pockets of the market are hungry for quality talent and offer great opportunity

- Businesses are optimistic: only 14% think the market will worsen, and organic growth is their top 5-yr focus

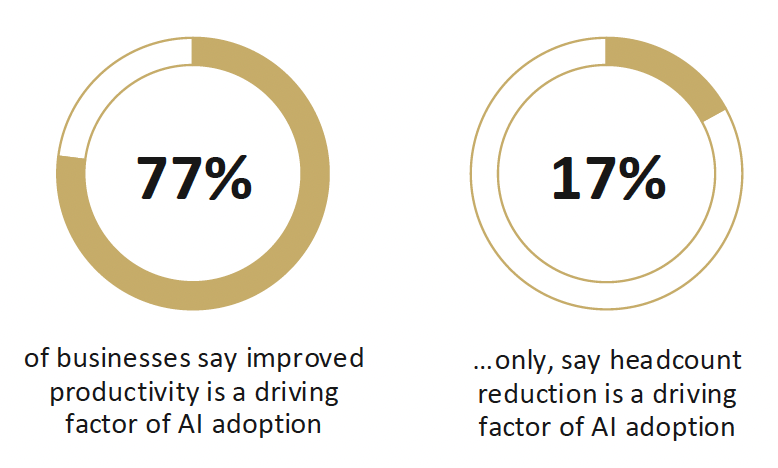

- AI is not driving job losses yet: Only 17% of businesses say headcount reduction is a driver of AI adoption.

The labour market is seen as impossible on both sides, but there is plenty of good news.

The data reveals a polarised market, not a closed one, with heightened extremes of supply and demand across sectors and skillsets. Specific roles remain in strong demand and specialist skills command a premium. And a structural shift sees talent migrating from major institutions to smaller, high-growth employers.

The report, which surveys both employers of tens of thousands of Australians and employees from across Financial, Corporate and Professional, and Tech and Transformation Services, found that last year’s redundancy waves at the major banks and financial institutions have reshaped the market. The resulting displacement has flooded the market with candidates, but there is significant opportunity in areas candidates are underweighting or overlooking.

Keegan Adams Managing Director Claire Tate said: “Major institutions are cutting and restructuring. But private wealth is booming, private credit is still maturing, non-bank lenders are expanding their market share where the banks won’t go, and a new generation of fintechs is building out teams.”

Investment teams in private markets are seeing demand outpace capacity, risk and compliance hiring also surges, driven by governance scrutiny.

Big shift to small end

In a spooked labour market, the perception remains that household names are the safe bet, offering stability and long tenures – especially amongst those newest to the workforce.

Tate explained: “8,000 jobs cuts at the big banks last year show that the biggest name is no longer guaranteed to be the safest bet. The risk calculus has shifted, and candidates need to update their assumptions.

“Much opportunity for career expansion sits beyond the giants – smaller firms can offer bigger roles, bigger opportunities.”

Within smaller organisations, remits are broader, leading to capability uplifts and faster career progression.

Dr Ben Hamer, accredited Futurist noted: “Curiosity is the thing that pays off over time, not a specific skill. The skills you learn today will be out of date soon enough. Curiosity is what helps you pick up the next one.

“With AI being heavily adopted across the big corporates and resulting in fewer job opportunities, we can expect a lot of the job growth to come from smaller firms most people haven’t heard of.

“The days of climbing one ladder at one company for 40 years are gone. The way people built careers a generation ago doesn’t really work anymore.”

AI

AI is also reshaping roles – often for the better. Over three quarters of businesses said improved productivity is a driving factor of AI, followed by efficiency and automation – just 17% said reducing headcount was a factor. The top areas for AI implementation are admin, analysis, and IT.

AI takes over more basic functions, freeing human agents to focus on what technology can’t replicate – higher order work. It elevates roles to become more strategic, with more resources to manage complexity and relationships.

Workers surveyed feel confident about adoption: only 1 in 10 feel they need to upskill. Unsurprisingly, Gen X and Tech & Transformation workers feel the most confident.

Hamer commented “”There’s a real gap in how we talk about AI at work. Recent NBER research found that two thirds of senior leaders use AI for about an hour and a half a week, and a quarter don’t use it at all. The people deciding how AI should change their workforce are often the ones using it the least, and it shows.

“AI has lowered the barriers to starting a business to the point where, for a growing number of young workers, building their own thing looks more attractive than joining yours. That’s a fundamentally different problem from the one most workforce strategies are built to solve.”

Labour market landscape

Across the last three years of this survey, difficulty finding a job continues to trend up.

Overall the private sector has seen negligible job creation since COVID and demand has slowed – a shift felt by both employers and candidates. More than 2 in 5 businesses are looking to fill fewer roles this year.

But at the same time, an astonishing 91% of employers felt it is just as hard or harder to find quality candidates as 12 months prior. Not surprising since their expectations have become increasingly exacting and specific in a plentiful market. Leading recruiters now approach high quality candidates with specific skills rather than filling roles based on inbound applications. This often leads to counter and counter-counter offers – as high as +40% of existing salaries.

Employee experience

Layoffs and restructure have sharpened candidate anxiety and an unsettled market sees many settle for safety. While most workers are looking to move (just 16% are happy to stay put), they often choose to stay in the end – with job security rising to top concern. Consequently, despite looking at roles the new normal, expected tenure has lengthened sharply, but out of fear, not satisfaction.

The constant hunt for new roles is, perversely, partly spurred by insecurity in their current role, but the major driven is dissatisfaction. 45% say their workplace culture has deteriorated in the last 12 months, with M&As, restructures, management changes, and performance pressures all contributing. Only 16% of workers are less stressed and just 11% feel less burdened. In addition to market factors, this is reflective of a long-term trend of rising work hours, with a 21% increase in monthly hours over the last decade.1

Approach to work

Worker perception is of an opportunities wasteland – and yet their expectations of hiring conditions haven’t shifted.

Only a quarter of workers are more willing to consider working in the office, despite the tough market conditions – and less than 7% are more willing to work a 5-day office week. Nonetheless, this year has seen some younger workers more willing to come into the office – to hold onto their jobs and to uplift their skills with training – with Gen Z much keener than their peers. In fact, less than 8% expect a drop in flexibility, job security, perks and non-financial benefits, or salary, in a new role.

Harmer noted “The war for talent was never really about talent. It was about what organisations were prepared to change to attract it. And that conversation is only heating up.”

1Feb 2016-Feb 2026, ABS 2026

To download a full copy of the 2026 State of the Workplace Report complete this form:

Published on June 3, 2026

Insights from our experts

From our blog

2026 State of the Workplace report reveals true market conditions

Job insecurity and polarised demand amount to a disorienting, sluggish job market. That’s what this year’s research found, published in the 2025/2026 annual Keegan Adams Financial Services Talent and Employment Report. Fear is driving an asymmetric job market, but forces are reshaping historic candidate movements, precipitating migration to smaller firms. Meanwhile, demand for very specific…

Latest news headlines on Australian labour market

From hiring challenges and talent shortages to salary trends across investment management and superannuation, Keegan Adams is at the forefront of conversations shaping the financial services, corporate services, and technology and transformation sectors. Drawing on insights from our latest 2026 State of the Workplace report, our team regularly contributes expert commentary and market intelligence to…

What does the future of work in Australia look like?

Last week, we were delighted to welcome clients, candidates and industry leaders to our annual Future of Work event, featuring renowned futurist and workforce expert Dr Ben Hamer. Attended by professionals from across HR, Talent Acquisition, People & Culture and business leadership eager to explore the trends shaping the future of work, the event offered…

Payments in ANZ: A Market Maturing – and What That Means for Talent

Payments in ANZ feels different in 2026 – and the recent RBA surcharge decision has only accelerated that shift. For years, the narrative was simple: growth, adoption, disruption. That’s still true — but it’s no longer enough. What we’re seeing now is a shift toward a more mature phase, where margin, regulation, distribution and execution…

The Shift in the Financial Controller Role Across Funds Management, Superannuation & FinTech

The Shift in the Financial Controller Role In recent months, we’ve observed a marked rise in demand for Financial Controllers across Funds Management, Superannuation, and FinTech sectors. Compensation data aligns with this trend, reaffirming that these roles now command higher salaries and expectations. Compensation Trends: What the Numbers Show Average base packages for Financial Controllers…

The Rise of Fractional C-Suite in Boutique Financial Services

Why private wealth and family offices are opting for flexible leadership Boutique financial services firms, particularly within Australia’s private wealth and family office sectors, are increasingly turning to fractional C‑suite executives. This model offers access to top-tier leadership without the long-term cost or commitment of a full-time appointment. For firms navigating growth, complexity, and regulatory…

Keegan Adams Recruitment Annual Event Recap – Boost Productivity & Retention in 2025

2025 Annual Report: The Evolving Workplace We are pleased to launch our 2025 Annual Report: The Evolving Workplace — our second annual report and a reflection of our ongoing commitment to providing a valuable resource to our clients and candidates each year. This year’s report goes beyond salary benchmarking, offering in-depth insights into how businesses…

The Evolution of Australia’s Superannuation Industry and Keegan Adams Recruitment’s Strategic Role

The Rapid Transformation of the Superannuation Sector The Australian superannuation industry is undergoing a period of rapid transformation, driven by consolidation, regulatory shifts, and the internalisation of investment management. As of the September 2024 quarter, total superannuation assets reached $4.1 trillion, reflecting a 3.7% increase over the quarter. This growth underscores the sector’s critical role…

Funds Management Distribution Market Update 2025

The Australian funds management distribution market is experiencing significant transformation as we move into 2025. In the face of evolving industry dynamics, fund managers are contending with a declining financial adviser base, institutional market consolidation, intensifying competition, fee compression, and shifting investor preferences. This update delves into the key trends, challenges, and opportunities shaping the…

Are you satisfied with your bonus?

In 2024, the Australian investment and wealth management industry is navigating a period marked by changing market conditions, regulatory shifts, and evolving workforce expectations. Bonuses and salary increases have become critical factors in attracting and retaining top talent, especially as firms strive to balance performance incentives with cost management amid uncertain economic landscapes. Trends…